With some variable rates higher than fixed rates, people are leaning towards fixed as their preferred rate.

Now that the spread between fixed and variable rates has largely evaporated, a majority of borrowers are once again opting for fixed-rate mortgages.

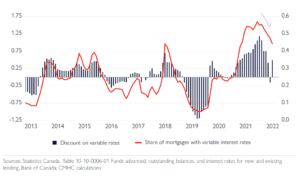

As of August, 44.2% of new mortgage borrowers chose a variable rate, down from a peak of 56.9% in January, according to the Fall Residential Mortgage Industry Report published by the Canada Mortgage and Housing Corporation (CMHC).

The shift coincides with the Bank of Canada’s rate hikes, which started in March and have progressively made variable-rate mortgages more expensive.

CMT calculations based on more recent data from Statistics Canada show the trend continued in September, with the share of variable-rate mortgages falling to 39% of new originations. That’s the lowest share since April 2021.

Share of mortgages with variable rates in Canada

Courtesy: CMHC

“The spread between variable and fixed rates has been trending downward after peaking in the first quarter,” reads the CMHC report. “Consequently, consumers’ preference for variable rates has decreased.”

The Statistics Canada figures also reveal mortgage borrowers are increasingly favouring shorter fixed terms as opposed to the traditionally popular 5-year fixed.

For new mortgages originated as of September by Canada’s chartered banks, just 16% had a 5-year fixed-rate versus 40% that had terms of one to four years.

Mortgage debt growth is slowing

These shifts are taking place against a backdrop of slowing mortgage debt growth, CMHC noted.

As of August, total mortgage debt stood at $2.05 trillion, an 8.8% increase compared to a year earlier. That’s down from a peak annual growth rate of 10.8% reached in February and marks the fourth consecutive month that the pace of growth has slowed.

Mortgage grow

Other insights into the mortgage market

CMHC’s report includes a wealth of additional findings relating to Canada’s mortgage market. Here are some additional highlights:

Mortgage originations in Q1 and Q2 of this year are down from the same period last year in all categories (purchases, refinances and renewals), but remained above 2020 origination levels.

The delinquency rates for credit cards, lines of credit and auto loans in Q3 were higher for consumers without a mortgage (1.69%, 0.66% and 3.04%, respectively) compared to consumers with a mortgage (0.49%, 0.19% and 0.31%, respectively).

Approval rates for both home purchases (71.3%) and refinances (85.6%) were down slightly in Q2 from a peak reached in Q4 2021. They both remain above pre-pandemic levels, however.

Among mortgage borrowers at alternative lenders, a smaller percentage were able to switch to a conventional lender in Q3 (67%) compared to Q2 (70%) and Q1 (72%).

Written and published by: Steve Huebl, Canadian Mortgage Trends

–https://www.canadianmortgagetrends.com/2022/12/the-popularity-of-variable-rate-mortgages-continues-to-fall/